4 Steps to a Must-Have Emergency Fund

Unemployment is the lowest it’s been in almost 20 years.

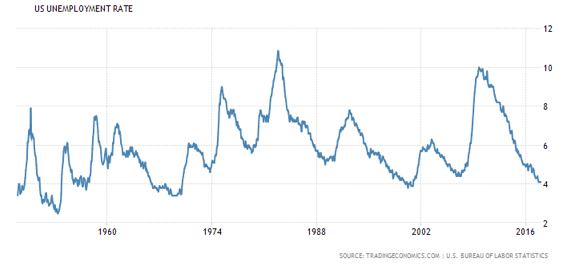

Take a quick look at this:

As you can see from the patterns on this chart, at some point the unemployment trend will reverse.

This isn’t some sort of secret, and it’s not a stock market prediction. It’s just a 500-foot view to show you how the economy and markets work: Boom and bust. Growth and contraction. High unemployment and low unemployment.

It’s as sure as the sun rises and sets.

The unfortunate thing is that those who are unprepared for a “bust” or don’t understand the economic cycle get hit the hardest.

Today, I’m going to tell you about one of the most important steps to building and preserving wealth…

I’m talking about building an emergency expense fund.

Why you should save

62% of Americans have less than $1,000 in their savings accounts and 21% don’t even have a savings account. That’s according to a recent consumer survey.

Those are shocking statistics.

Let’s see how a “bust” plays out for someone in this demographic, alongside someone who is ready for economic downturns.

Person A and Person B are both progressing along in their careers. Person A has no savings account and $10k in credit card debt. Person B has a savings account with three months of living expenses stashed away and no debt.

Now, it’s important to note that on the surface, there’s almost no recognizable different between Person A and Person B. They are both climbing the ladder in their respective careers and working to invest time and energy in what’s important to them. They have families, a car, a house. The American dream, right?

But Person B has set aside a little amount each month for the past few years in case of an emergency. Person A has, well, just spent money—often before they get it in their checking account.

It doesn’t take a genius to figure out which of these individuals would survive the blow of losing their job during the next economic downturn.

If Person B happens to lose their job, they have time. Time gives them options. They can move to a new location where jobs are more plentiful; they can stay where they are and devote time to finding the right job for them; or they can agree to stay at home for a while while their partner/spouse works. Meanwhile, they can collect unemployment to help with the bills or take on some side projects/freelance work to supplement household income.

You see, people who have options always have the advantage.

But what about Person A? Well, that’s a much uncomfortable story. If they lose their job—with no severance—they have to scramble to find income. They take any job they can, just to make ends meet. Their quality of life plummets. They don’t have time to look for better-paying, more meaningful work. And their health takes a nose-dive because of the rapid ramp-up in stress and frenzied activity.

Which scenario would you choose—an option-lined though unfortunate layoff, cushioned by a three-month emergency fund, that might lead to better opportunity; or a chaotic life lived paycheck to paycheck without the hope of overcoming the burden of incessant financial obligations?

Yep, Person B it is.

How much to save

Now, I just picked three months of living expenses in this example. It’s a common number thrown around by financial experts. Investment firm Vanguard recommends 3-6 months depending on your industry or other situation. Finance guru Dave Ramsey recommends 3-6 months as well.

If you’re a business owner and you listened to Craig and Bedros’s most recent Empire Podcast, Bedros says entrepreneurs should only keep 2-3 months of living expenses in the bank. Business owners should live on a razor’s edge and invest their profits back into the business.

Why? Here’s the gist: If you can’t make something happen and start earning money in three months, you’re not going to do it in 12 months.

The same applies to your finances, which is why 3 months is the golden number. If you can’t land a stable, financially sound job 3 months after layoff, you’re not likely to—unless your circumstances change significantly.

Keep this in mind as you build up your fund.

Regardless of whether you save for three months or a year, however, an emergency expense fund is about giving yourself options, preserving wealth without increasing debt, and not putting your family under financial stress.

It doesn’t take much to get started, either. Here’s an example of how much you can save in two years if you save $25, $50, or $75 each week:

Source: Vanguard

Source: Vanguard

And keep in mind that this fund isn’t just for a layoff crisis. It could be for an emergency room visit, when the A/C goes out in your car, or when your leaky roof finally needs to be replaced.

How to save

There are four simple steps to this, so there’s no reason not to start saving today:

- Take some time this week and create a critical living expense budget. There’s no magic formula for setting this up (although the linked Quicken guide well help). It takes time and a little discipline, but will give you concrete numbers to start with.

- Add up all of the expenses you need for a month. This is how much cushion you want to have in the bank to get by for one month.

- See if you can save up a month of living expenses in the next six months or so. I did this by finding luxuries I didn’t really need. These add up. So, for instance, I uncovered some magazine and app subscriptions that having been adding up in the background and cut them. Instead of just spending that extra money, I moved it to a savings account.

- Your second, third, and fourth months will be easier once you have a system down. Adding this savings to your monthly budget helps, by the way, so consider inserting it as a line item (and maybe dropping a few Starbucks runs or shopping trips to make room).

Where to save

You’ve started to bring in money to your emergency fund. Congratulations!

But do you keep it in your checking account? No; too easy to spend. Do you stash it in your primary savings account? Bad idea; you might siphon some of it off for vacations and minor house projects.

My tip: Start a new, emergency fund-only savings account. Drop it all in there and don’t look at it.

You might be wondering if there’s a better way to get returns on the money you’ve saved up, but don’t worry about that. Your goal isn’t top interest rate returns or profit; it’s about having a secure financial cushion in times of crisis. And if you’re tempted to invest your emergency fund dollars, consider this: Every potential money-making investment has a risk that balances it out. Just think back to the ’90s dotcom reckoning; plenty of once-booming behemoths fell into bankruptcy and oblivion. You don’t want your money wound up in that uncertainty.

Put simply: The whole idea of an emergency fund is to create something unshakably stable; if you invest it, you run the risk of the market turning it into nothing.

Oh, and make sure your bank is FDIC-insured. That just means that a single account is federally insured up to $250,000. So, if the bank were to fail, you would get everything up to $250,000 paid back to you by the federal government. (Most big banks are FDIC-insured, but some small or local banks may not be. You can learn more about FDIC insurance and coverage here.)

At the end of the day, there’s no reason NOT to start an emergency fund. It will give you and your family peace of mind, knowing that the future won’t collapse if crisis hits. All it takes is a modest $25 a week to get started—the same cost as 2 movie tickets or 5 Starbucks lattes.

If you ARE ready to invest and are keen on getting the best advice available in the market today, subscribe to our industry-leading Wealth Confidential Newsletter.

If you ARE ready to invest and are keen on getting the best advice available in the market today, subscribe to our industry-leading Wealth Confidential Newsletter.

Each month, we share investment tips from real estate moguls, business owners, VCs, entrepreneurs, and self-made millionaires. There’s nothing like it out there—and worth every penny. >>> Subscribe today!

Chad Champion

Chad Champion, The Champion Investor, is focused on educating people on how they can create monthly income using a low-risk, conservative options strategy and learning the skills they need to become better investors. He has a finance and investment management background with an MA in investment management and financial analysis and an MBA in financial management. Learn more at thechampioninvestor.com