How to Become a Millionaire

You’ve wondered what the person sitting at the desk next to you is making. How they afforded that all-inclusive trip to the Bahamas and still afforded a new car.

But did that person sitting next to you just inherit some money? Are they bleeding through an old trust account? Or maybe just burning through savings? Or worse, one of those horror stories you hear about racking up $60,000 of debt on credit cards.

Perhaps your boss is giving them all those raises you’ve been missing out on the past few years.

You can’t ask…

Money is a taboo subject.

It’s personal and you’d be better off ignoring those neighbors.

Instead, we are influenced by these neighbors and it has left many people broke just a few years before retirement.

A recent study of Americans between the ages of 50-64, showed that about 51% didn’t even have a retirement account. And those that did have an account, the average balance in all of their retirement accounts was $46,032.

Now maybe, that seems like a lot to you, but a recent Aon Hewitt study said that you would need at least 11 times your final working salary if you plan to retire and maintain the same standard of living. And ABC reported that an average retired couple would need over $220,000 just for medical expenses during retirement.

This paints a scary picture for the future.

But a few simple steps can make sure that you have the right amount of money available for your future.

I know, I know. You can tell me that you don’t control whether your company gives you a raise, if the stock market goes up (or crashes) or how government taxes or benefits will change.

Many things are actually out of your control. Trying to control these things can lead to paralyzing decisions that result in no action. So rather than falling victim to these external factors which are outside of your control, let’s figure out what things you can do to take the reigns of your own financial future.

There are 4 things you control in your financial life:

1. Spending

2. Saving

3. Timing

4. Risk

They are THE critical factors to your success. Focusing your energies on areas within your control will make you realize that you are empowered to build your own wealth. It is no longer a desire to wait for a raise, win the lottery, or for the stock market to make you more money.

As grim as the situation may be, there are more millionaires in the U.S. than ever before.

So how did they get there? These millionaires weren’t lucky or didn’t get rich quick by luck (well maybe one or two of them). Instead, they focused on these four things within their control.

Planning ahead, you can quickly see how easy it is to become a millionaire.

If you take $10 per day saved it in an investment that earned the average return of 8%. About the cost of a daily lunch or your monthly cell phone and cable bill…maybe less. We will focus how to control spending in a future issue, but you know it can be done.

If you started that in your 20s, you’d be a millionaire in 39 years. But say you were a little more aggressive and saved $20 per day and invested it at 12% return. You could be a millionaire in 24 years.

The reason is because savings can compound.

Just have a look at how saving a small amount per day can impact your time until you can become a millionaire.

The most interesting part of the chart is to see the interest that grows for you. The longer the money is in savings, the larger the balance becomes to pool its interest. By the time you are a millionaire, the first month you saved $300 will become worth $6,951.07 in the 39 years it takes to be a millionaire.

| Savings per day | Rate | Total Saved | Total Interest | Time to $1 million |

| $10 | 5% | $195,000 | $807,244 | 54 years, 2 months |

| $10 | 8% | $142,200 | $862,412 | 39 years, 6 months |

| $10 | 12% | $106,800 | $899,607 | 29 years, 8 months |

| $20 | 5% | $299,400 | $703,319 | 41 years, 7 months |

| $20 | 8% | $225,600 | $779,015 | 31 years, 4 months |

| $20 | 12% | $173,400 | $830,812 | 24 years, 1 month |

| $30 | 5% | $374,400 | $627,655 | 34 years, 8 months |

| $30 | 8% | $288,900 | $715,404 | 26 years, 9 months |

| $30 | 12% | $225,900 | $777,823 | 20 years, 11 months |

Is saving an extra $10 or $30 a day possible?

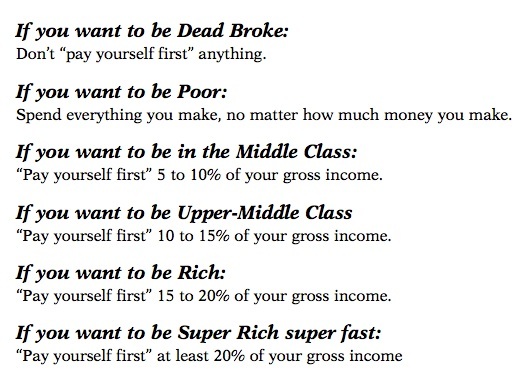

The strategy personal finance expert David Bach recommends that the first hour of every workday is paid to yourself.

The average American worker only saves 22 minutes of their salary per week. It’s no wonder there is such a lack of savings. If you are making $10 an hour, you should be saving $10 per day. If you make $50 an hour, it should be $50.

Paying yourself first makes sure you are properly saving. Because in reality, this is the only way to wealth that is 100% within your control.

Sure, there may be other ways. You can inherit wealth, marry into it, or win the lottery. But none of those ways are in your control.

That’s why making a conscious decision to save by paying yourself is critical to growing your wealth.

There are some simple rules to create prior to setting up a system to pay yourself.

1. To save properly, it’s best to plan then allow it to be automated.

It’s too easy to spend money that’s in an account or feel comfortable making large purchases when you see cash that is sitting idle. Instead, when you put saving on autopilot, you’ll soon view the entire account as a savings account that is intended to increase your wealth.

2. The number one rule of this new account is to take NO WITHDRAWS to any account that you spend out of. You may transfer funds from this account to another wealth generation account once per year. You’ll likely need separate accounts to invest the funds.

Other than those transfers, this account is not where you save for large purchases or vacations. This isn’t an emergency fund. This is a wealth fund. The balance in the wealth funds should increase each year.

3. These funds should be invested in low risk investments. This is the only way to make sure the account balance increases each year.

Too many people look at wealth as an all or nothing game. We know you can’t coupon your way to it, but it is a gradual, long-term project.

If you think you will strike it rich with high-risk investments, this account could easily go down in value (possibly to zero).

Once again, these savings are a wealth account, not an investment account. With the power of compounding, you need to only earn 5% per year to become a millionaire. If you aim for unrealistic returns, you put the account for unnecessary ups and downs.

This account is for bonds, dividend paying stocks, and investments with predictable, steady cash flows.

Don’t view it any other way.

[Ed Note: Jeff Schneider is the COO of Early to Rise. He has worked as a regional controller for a Fortune 50 company and built a financial consulting business. Aside from the normal lemonade and doughnut stands, he made his “first sale” for his own product when he was 16. In his most recent venture, he used his CPA training to consult with thousands of individuals on the best way to protect and invest the wealth in their retirement accounts. Jeff now writes a monthly personal finance article from his experience in the blueprint for financial freedom, Financial Independence Monthly. Click here to learn more.]